Sundry Photography/iStock Editorial via Getty Images

Recently, I completed divesting shares in ASML Holdings (NASDAQ:ASML) and Taiwan Semiconductor Manufacturing Company (NYSE:TSM). I absolutely hated selling these companies because I think so highly of them. They have great managements and dominant positions in the semiconductor industry. So why did I sell? Well, that’s what I’m going to try to explain.

A Note On My Strategy For The Rethink Technology Portfolio

I’ve espoused a buy and hold strategy for the Rethink Technology Portfolio, identifying companies that I thought were both undervalued and had great long term growth potential.

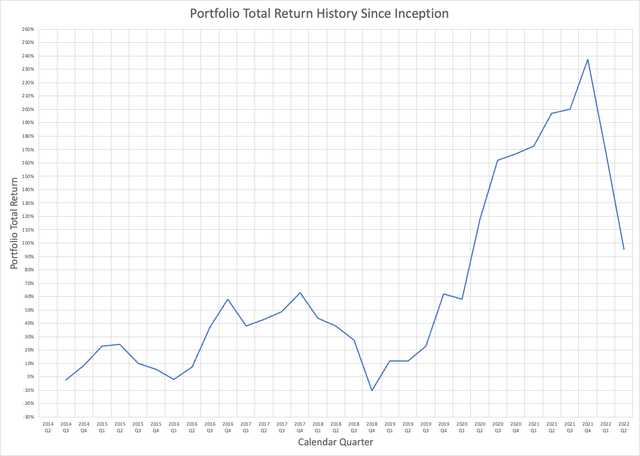

I’m not saying that this was always the best strategy, but it worked well for me and the Portfolio. Even with the steep downturn this year, the Portfolio total return is better than 90%, where total return percent is defined as:

Total Return Percent = (Current Portfolio Value – Portfolio Cost) / Portfolio Cost

And I stuck with this strategy even when the Portfolio total return turned negative in late 2018:

In late 2018, I just didn’t think the panic that we were seeing in the technology sector was justified. There were fears of a recession that didn’t come to pass, and the sector gradually recovered until the COVID recession of 2020, which the Portfolio hardly noticed.

When the downturn started this year, I was still determined to continue accumulating and did so until the Russian invasion of Ukraine. I had been willing to wait out another recession, and even endure further losses to the Portfolio, but the Ukraine war increased risk in many areas, as I explain below.

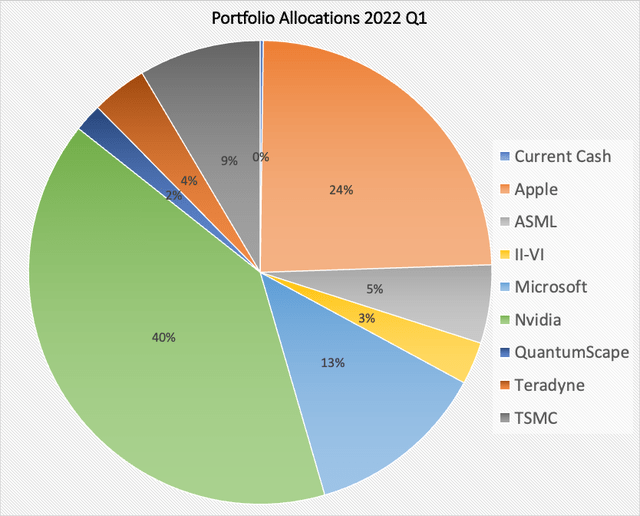

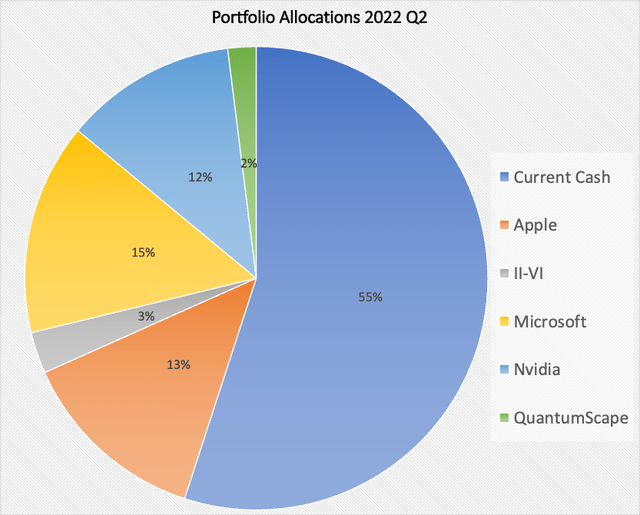

I’m currently carrying a lot more cash than I ever would have done before, as I show in the following charts. The Portfolio allocations as of the end of 2022 Q1:

In addition to closing positions in ASML, TSMC, and Teradyne (TER), I’ve reduced positions in Apple (AAPL), II-VI (IIVI), and Nvidia (NVDA):

Questions About The Global Semiconductor Shortage

One of the interesting features of the semiconductor shortage is that it has mostly impacted semiconductors that use so-called “legacy nodes”, typically 20 nm and larger, whereas advanced semiconductors such as processors by AMD (AMD), Nvidia, and Apple use processes in the range of 5-7 nm. Most of these legacy node semiconductors are for power regulation, mixed signal devices that include digital and analog sections, microcontrollers for industrial applications and automotive, and radio frequency (RF) devices.

It was the automotive industry that was starting back up after COVID related shutdowns that was first affected in late 2020 and early 2021. But there was something strange about that. The auto industry wasn’t ramping exceptionally high volumes at this time but simply trying to get back to pre-COVID production levels. And they were finding that very difficult.

The mystery deepened into 2021 as shortages did not relent, but production on the legacy nodes was running at capacity. Where were the semiconductors going?

This led to a very interesting exchange during ASML’s 2021 Q3 earnings conference call. Sandeep Deshpande of JP Morgan asked:

I mean Peter, you saw a very strong increase in your orders in this cycle, in Q4 last year, you saw a big step up. And I mean even today now, there are shortages in the semiconductor industry. How are — I mean, given that you have that visibility in terms of the wafers flowing through your equipment as such, have you seen additional wafers flowing today versus say Q4 last year through your equipment to say that there is much more capacity today versus in Q4 last year? And why are we still — there are such big supply chain bottleneck, including for yourselves and for many others in the — and particularly related to the semiconductor industry?

ASML CEO Peter Wennink replied:

Yes. Sandeep, I mean, you’ve been around a long time and you asked the million-dollar question. So — and the real answer is we don’t know. We have some indications and some ideas and yes, you are absolutely right. The wafer out capacity today is a lot larger than it was in Q4 2020, that’s true. And still, we see these shortages.

Now, I spoke to a very large customer and basically asked the same question. They actually said, you know, Peter, we don’t know either, because somehow we haven’t been able to connect all the dots that actually are the underlying drivers for this demand.

Now, there are some rumors out there that the brokers and the distributors are playing a devious role here because they stock up all the inventory and drive up the prices, but I don’t believe that that much. Yes, there will be some of it. But even for the very large customers like the smartphone makers that are direct customers to the semiconductor makers and have nothing to do with the distributors, yet, they are in shortage also.

For ASML’s “large customer” read TSMC. TSMC is ASML’s largest customer, and they have a very close working relationship. The fact that even TSMC didn’t know where the demand was coming from is not all that surprising.

TSMC sells wafers to the fabless semiconductor makers who then sell their components to end customers. TSMC’s customers wouldn’t share information on the end customers or what and how much they were buying.

Wennink went on to cite the usual suspects to account for the shortage: greater silicon content in connected cars, the growth of IoT, and adoption of 5G mobile devices. But even he admitted that he hadn’t “connected the dots”.

I believe that another source of pressure on the semiconductor industry has been from crypto mining. Crypto mining is just transaction processing for currencies that use block chain technology, and as such, it’s far more energy intensive than traditional credit card processing. Last year, I calculated that the energy consumed just for Bitcoin and Ethereum mining was equivalent to the output of 6 gigawatt-class nuclear reactors.

And all of these mining rigs require power supplies to deliver all that power. That means voltage regulators, power controller ICs and microcontrollers, in addition to the ASICs or GPUs that do that actual mining. Just the sorts of things that have been in short supply.

And of course, the consumer GPU shortage has been a source of consternation for more than a year. Nvidia’s Ampere RTX 30 series graphics cards have been in short supply since they were released in September 2020. Only recently, have prices for consumer GPUs started to come down to near-list.

I have estimated that crypto mining contributed as much as 23% of Nvidia’s Gaming segment revenue as of its fiscal 2022 Q3 (ending October 31, 2021). The recent improvement in GPU supply seems to correlate with factors that would reduce mining GPU demand.

First of all, the creators of Ethereum have been promising for some time to move to a “proof of stake” approach to transaction processing that would greatly reduce computational requirements. Ethereum’s creators have acknowledged the detrimental environmental impact of traditional crypto mining.

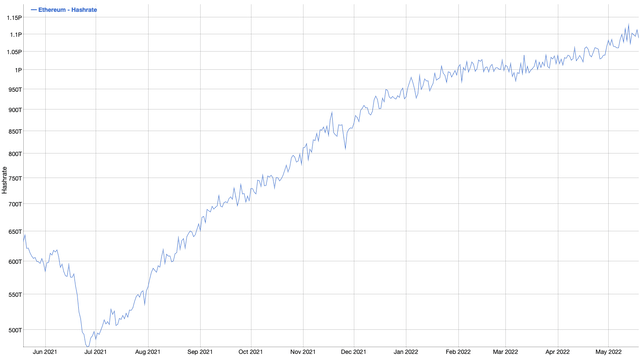

In anticipation of this transition, Ethereum miners are likely not investing in any more mining capacity. This seems to be the trend since the beginning of the year which has seen Ethereum mining capacity, measured as a hash rate, leveling out. Bit Info Charts tracks the collective mining capacity of various crypto currencies, and their data on Ethereum supports this trend:

Source: Bit Info Charts.

I have speculated that Russia might also have contributed to the semiconductor shortage:

Putin seems to be a chess player, who plans many moves in advance, and who spends a great deal of effort trying to anticipate the moves of his opponent. I believe that Putin has always known where he was going on Ukraine since the Crimean invasion of 2014.

Preparations for the invasion of Ukraine this year probably began in earnest at least a year ago. Putin could easily anticipate that the response of the West would be economic sanctions, which could include denial of access to advanced semiconductors, as China had already been denied.

The obvious mitigation for this would be to stock up in advance, especially for militarily important semiconductors, including CPUs, GPUs, and power semiconductors. These would all be important for the guidance systems of smart munitions such as smart bombs, ballistic missiles, and cruise missiles.

This is all speculation of course, but I have felt that the crypto impact, as large as it seemed to be, was nevertheless not enough to account for the severe shortages. Also, I noted that the recent improvement in GPU availability just happened to coincide with the imposition of sanctions following the Ukraine invasion. Coincidence? Perhaps.

But I think that investors should consider that much of current semiconductor demand may go away in the near future, ending the shortage before planned capacity expansions take place. Both TSMC and ASML are planning capacity expansions, not merely for advanced nodes, but for legacy nodes that normally would see no expansion. Normally, production on legacy nodes declines over time, so there’s no need to expand production capacity.

I doubt that the financial impact of planned expansions would be that severe, even if they had to be halted in mid-stream. ASML already has a huge backlog, and new orders can take over a year to deliver. The order lead times for new semiconductor equipment may actually help if TSMC has to cancel its expansion plans. And ASML has made clear that its expansion plans mainly rest on its suppliers, so that minimizes ASML’s risk if it has to curtail its own capacity expansion.

But there’s the longer-term concern about whether the growth expectations for the semiconductor industry are realistic. They may not be. My expectation is that we’ll see semiconductor supplies return to normal this year, well ahead of expectations.

A number of factors feed into this expectation. We have a looming recession which will almost certainly drive down demand for consumer electronics and other items that make extensive use of semiconductors such as automobiles.

Continuing stock market declines seem to be driving investors out of speculative investments such as crypto. The consequence of crypto declines appears to be a reduction in mining activity and decreased demand for new mining rigs.

And finally, sanctions on Russia may have exposed a heretofore unidentified source of semiconductor demand. All of these factors appear to be converging to drive down demand for semiconductors at a time when industry leaders such as ASML and TSMC are poised to reap the benefits of what is assumed will be a burgeoning semiconductor industry.

Putting The Portfolio On A War Footing

If the only concern I had about ASML and TSMC was that growth expectations might be overblown, I wouldn’t have sold them. They’re both excellent companies with great track records of innovation and profitability. It was the war in Ukraine and the danger of escalation of the conflict that tipped the balance in favor of selling.

As I informed subscribers when I started selling Portfolio companies:

I now consider a particular scenario in Ukraine a realistic possibility. In this scenario, Russia attacks one or more Ukrainian cities with tactical nuclear weapons. The most likely target would be Kiev.

This would leave NATO with having to decide how to respond. NATO and the U.S. have threatened “severe consequences” if Russia were to use nuclear weapons, but haven’t specified what those consequences would be.

I think it likely that Putin has come to the conclusion that he can’t win the war without the use of nuclear weapons, while at the same time believing that if the use of such weapons was confined to Ukraine, NATO would not retaliate in kind.

Probably, the best way to deter Putin would be to make clear that the use of nuclear weapons would be considered an attack against NATO, since nuclear fallout would almost certainly spread to neighboring NATO members. But there doesn’t appear to be consensus within NATO to draw this line in the sand, and Biden doesn’t appear to be willing to act unilaterally.

Thus, Putin may well be correct that NATO would stand by, perhaps imposing more sanctions, but unwilling to widen the war. In this scenario, Putin achieves “victory”.

It’s shocking to think about nuclear warfare, but until recently, a major land war in Europe would have been unthinkable as well. And unfortunately, Russia’s recent military reversals in Ukraine do not make the nuclear option less likely.

I can’t begin to assess what the probability is of Russia using nuclear weapons, but I can easily imagine the consequences. World markets would go into freefall.

In risk management, one is taught to give equal weight to probability of occurrence and severity of consequence. Even if the probability is small, if the consequence is severe, then the event or condition is considered high risk. And this is what I think we have with the Russian nuclear option.

Unfortunately, ASML, as a European company, looks particularly vulnerable, both from the standpoint of investor reaction, as well as direct impacts to the company should the war widen beyond Ukraine’s borders. As such, disposing of ASML became essential risk management to adjust to the new war time reality. And I could hardly complain about my total return of 242%.

I viewed TSMC as less at risk, and I’ve written that Taiwan is in a more secure position than Ukraine. But less risk is not zero risk. TSMC still has all of its leading-edge semiconductor production in Taiwan.

Even if the People’s Republic refrained from invading Taiwan, it could still inflict severe damage to infrastructure through missile attacks. Since we’ve denied Chinese access to advanced semiconductors produced by TSMC through export restrictions, the Chinese might decide to level the playing field by destroying TSMC’s advanced fabs.

Once again, the probability of such an event may be low, but the consequences are severe. When you add that to a future semiconductor slump that might last years, TSMC became another profit taking opportunity, with a total return of 120%.

Investor Takeaways

So, one takeaway from this is that I’m pivoting away from companies in vulnerable geographic areas. ASML has all of its production concentrated in the Netherlands, with suppliers throughout Europe. TSMC has most of its production and all of its advanced node production in Taiwan.

Another takeaway, and perhaps the most important, is that investors, especially tech investors, are now living in a world of unprecedented risk. Runaway inflation, food shortages, semiconductor shortages (at least for now), recession, COVID, and a major land war in Europe. I would never have believed it possible.

Even with all that, I’m not going to pull completely out of equities. But I am refocusing on what I consider core assets. These are what I call the “new paradigm” companies that have moved or are moving away from the traditional commodity PC model. These are Apple, Nvidia, and Microsoft (MSFT).

These companies are not immune to world events, of course, but they’re probably as safe as it gets in the tech space. I’m also seriously looking at adding a defense contractor or two to the mix, such as Raytheon Technologies (RTX), maker of the Patriot missile defense system and Phalanx close-in weapons system.

Phalanx CWIS. Source: Raytheon Missiles & Defense.