da-kuk/E+ via Getty Images

Overview

This article will highlight the differences in last year’s 2 rallies in 10-year yields and its implications for people invested in Bitcoin (BTC-USD) and other cryptocurrencies. I will argue how the February rally was largely a result of heightened inflation expectations (which turned out true later on in the year), while the December rally was a result of the Fed’s tapering program and hawkish pivot, likely for the next few years.

Finally, I will answer how these 2 rallies are related to the correlation between Bitcoin and tech names with unsustainable multiples that suffered for much of 2021, with the ARK Fintech Innovation ETF (ARKF) as the poster-child ETF of these companies. This will highlight the very real risk to cryptocurrencies such as Bitcoin going forward and negate much of its gains in 2021.

Part 1: The February Rally In Bond Yields

TradingView

(Purple – US 10-yr yield; Blue – US 90-day LIBOR; Yellow – US Inflation Rate YoY)

As can be seen, the main reason for the February rally was an increase in inflation expectations. In that respect the yields were actually a decent leading indicator, as inflation subsequently rose steeply before plateauing. This was also supported by many strategists and economists as it was more or less the consensus argument behind the rally.

Part 2: The December Rally In Bond Yields

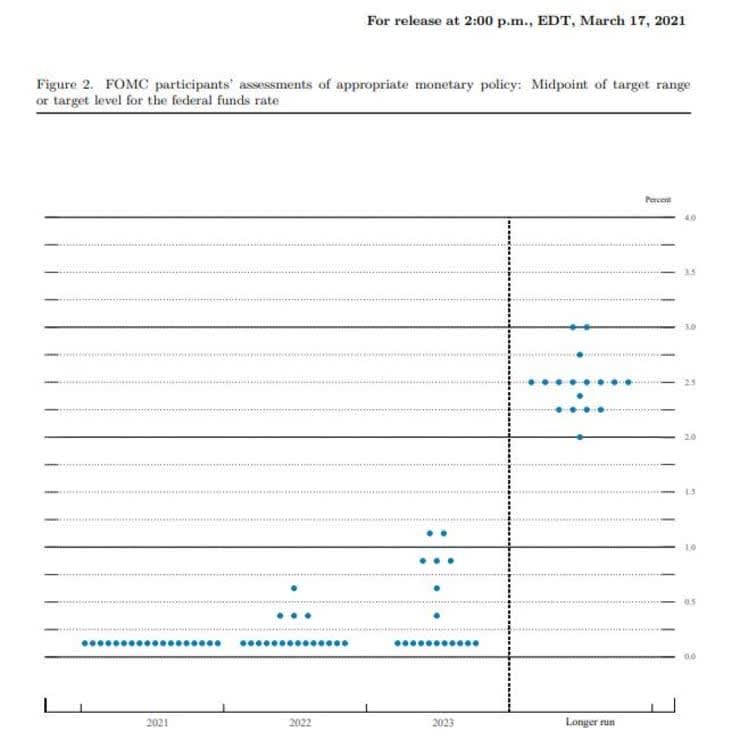

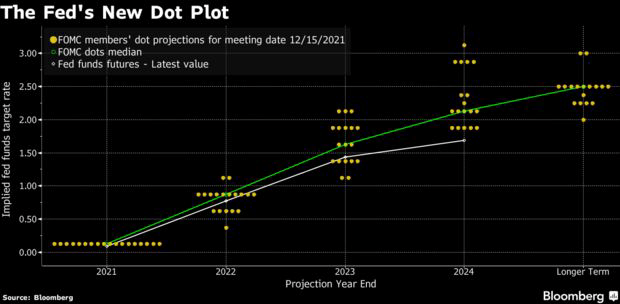

Following one of the most hawkish pivots by the Fed in the past few years in its December 2021 FOMC Policy Statement, the 10-year bond yield once again surged to 2021 all-time highs. Using the 90-day LIBOR, you can see how banks are already trying to price in multiple rate hikes in 2022 alone. You can also see the drastic change in the Fed Dot Plot from March 2021 to December 2021.

Dot Plot in March (CNBC) Dot Plot in December (Bloomberg)

It is likely that 10-year yields will go past 2% in 2022, which is what is predicted by many strategists and economists.

Bond Yields As A Leading Indicator For Bitcoin? The Answer Is Not That Simple

TradingView

(Purple – US 10-yr yield; Red – BTC/USD)

If you were to look at the correlation between 10-year yields and Bitcoin, in the rallies of February and December, you would see 2 completely different scenarios. One where they share a positive relationship (February) and another where they share a negative relationship (December). While this may seem unusual, it can explained by the previous chapter where I highlighted the reasons for the 2 rallies in bond yields.

For all the idiosyncratic benefits that cryptocurrencies such as Bitcoin offer such as decentralisation and anonymity etc., I prefer to look at crypto from an extremely reductive yet big-picture point-of-view: in the extremely adaptive capital markets where one dominant idea is likely to influence the decisions of individual agents to form a collective trend, cryptocurrency is nothing more than an inflation hedge, and its 2021 performance is a case in point of that.

Going back to how the 2 yield rallies tie in with Bitcoin, it is clear for the first half of the year, where bond yield movements were in tandem with inflation expectations, that the 10-year yield would be strongly correlated with Bitcoin prices, as a rise in bond yields would signal greater future inflation, strengthening Bitcoin’s value proposition as an inflation hedge.

For the second half of the year, as I have previously highlighted how the reason for bond yield movements were now due to expectations in the Fed’s monetary policy, it is once again clear that Bitcoin would naturally move inversely with bond yields since a rise in bond yields would signal higher future interest rates, meaning expectations of lower money supply and velocity of money, which would naturally tamper speculation in Bitcoin and other cryptocurrencies.

Therefore, in the grand scheme of things and in the long run, for all the ways that cryptocurrency can “change” the world, cryptocurrency in the capital markets is mainly an inflation hedge.

Is Bitcoin Still An Uncorrelated Asset?

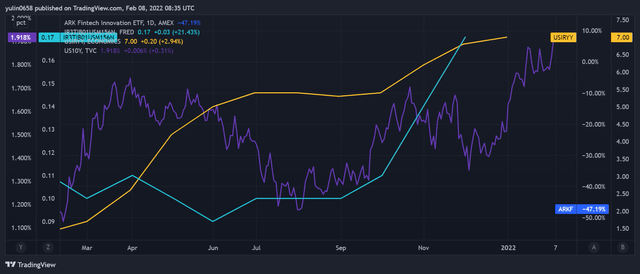

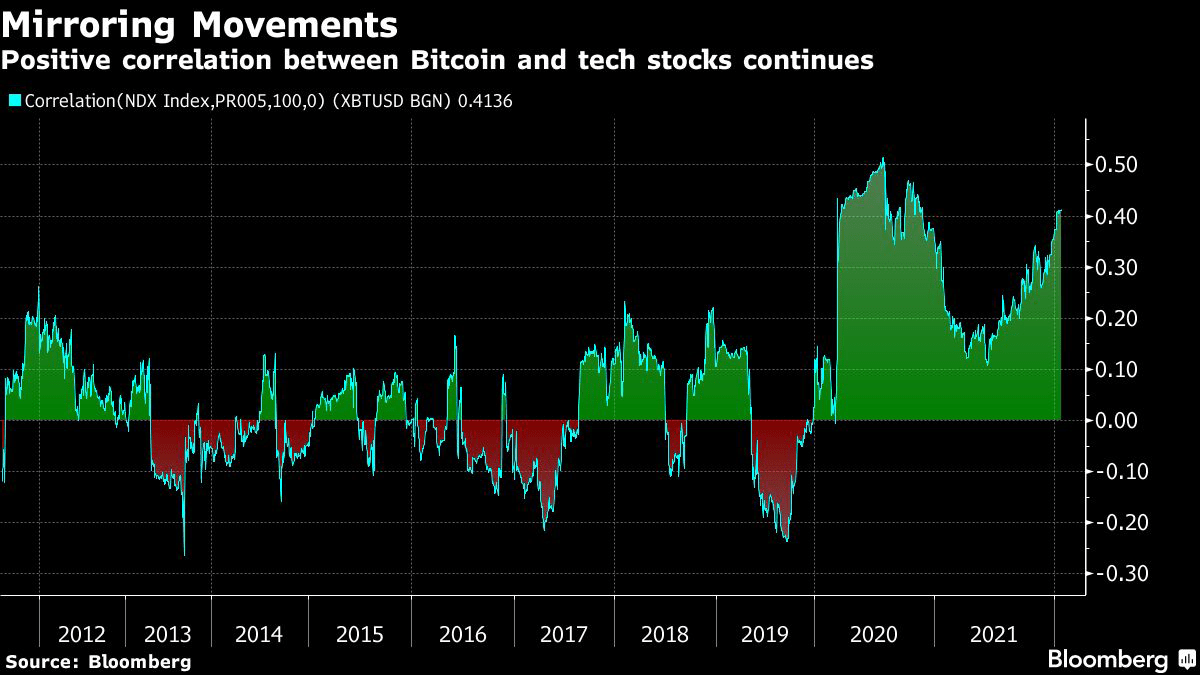

At the very start of Bitcoin’s 2020 rally, many asset managers highlighted how cryptocurrencies such as Bitcoin offer a largely uncorrelated asset to the broader S&P, helping to hedge and diversify portfolios. In my opinion, however, to say that Bitcoin is still uncorrelated with the broader market would be inaccurate. More worryingly, it is Bitcoin’s correlation with tech stocks specifically that has been increasing, which is concerning given that tech stocks will likely be the worst hit in 2022 by the Fed rate hikes.

Bloomberg

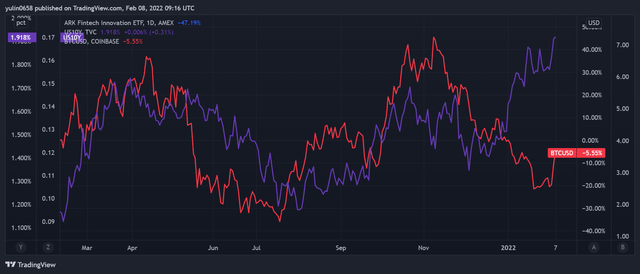

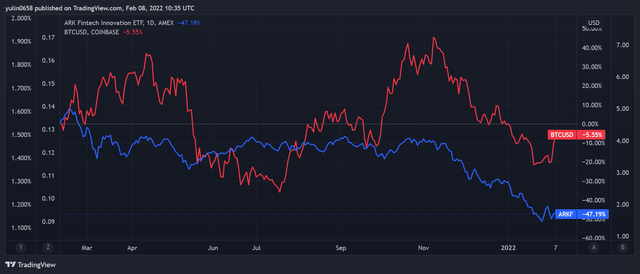

Just to use an example to give a clearer image, I will be using the Ark Invest ARKF ETF, part of the Ark Invest catalogue of ETFs that have come to symbolise today’s cash burning companies with expanded multiples and growth rates that often miss management guidance. You can see how the correlation between Bitcoin and ARKF becomes more prominent in the later half of the 2021, as the macroeconomic narrative shifts to a hawkish Fed.

TradingView

Conclusion: Going Forward

Bitcoin, cryptocurrency and the broader De-Fi space will no doubt bring benefits to society in terms of security and convenience. However, as investors, it is important to delineate tangible factors that will affect its performance in the capital markets, rather than focus on things like societal benefit etc.

In this article, by taking a brass-tacks view of cryptocurrency, I have highlighted how Bitcoin performs in 2 fundamental factors: its sensitivity to economic conditions and its correlation with the broader markets. Going into 2022, it is likely that the macroeconomic headwind provided by the Hawkish fed will be far too strong for any idiosyncratic tailwind, such as the adoption of Bitcoin as payment by some big company.

Credit: Source link