They’ve all, in one way or another, gotten involved with blockchain technology – a fairly new, complicated and frequently surreal invention.

If you’ve never heard of the term “blockchain”, you might well have caught mention of cryptocurrency or NFTs.

But if this is all brand new to you – and you can certainly be forgiven if it is – fear not!

Keep reading for a helpful, fluff-free guide to everything blockchain.

What is a blockchain, and how does it work?

Blockchain technology actually dates back to the early nineties, but wasn’t used all that much until the late 2000s.

Simply put, it’s a method of storing digital information.

Think of an Excel spreadsheet, or any table of information: You get a series of columns and rows with different labels, and information is inserted accordingly.

In a blockchain, information is instead stored as chunks – or blocks – that are linked together in chronological order, forming a chain. Each of these blocks contains not only information, but an identity marker, a unique piece of code called a “hash”.

Each block contains its own hash and the hash of the previous block in the chain, and it’s this that links them together.

The hash identifies the block and its contents, and will automatically change if the information in the block changes – meaning that, in theory, you’ll always know if it’s been tampered with in some way.

READ MORE: The Celyn, Wales’ new currency set to launch this year

To generate the hash, a computer – or, more often, a set of computers (more on this below) – needs to solve a cryptographic puzzle at a certain level of difficulty.

When that puzzle is solved, you get both the hash and something called “Proof of Work” (PoW) – proof that the right amount of effort has been used to find the answer – and this confirms that the stored information is valid, and hasn’t been messed with.

Most blockchains are “decentralised”, meaning that a network of multiple computers is involved in the process of calculating hashes. These blockchains are considered permanent, unchangeable records, with information spread out rather then held in a single, central location.

Not all blockchains are bad for the environment, but the more computers in its network, the harder the hash puzzle becomes, and the more computing power it takes to find the answer – which can mean considerable energy use.

This year the Welsh Government launched a Blockhain Challenge Fund to “demonstrate the potential of the blockchain”.

What about cryptocurrency?

Not all blockchains are used for cryptocurrency, but the most famous ones – like Bitcoin and Ethereum – certainly are.

With cryptocurrency, the blocks store information about monetary transactions – who gave what amount of cryptocurrency to whom.

Confusingly, Bitcoin doesn’t actually involve any physical coins!

Confusingly, Bitcoin doesn’t actually involve any physical coins!

The hash code and the PoW here are what gives the currency value – they confirm that the transaction took place and was valid, without the need for traditional money and the involvement of banks or other financial institutions.

The concept of decentralised cryptocurrency was first detailed in a 2008 paper – “Bitcoin: A Peer-to-Peer Electronic Cash System” – by an unknown person using the pseudonym Satoshi Nakamoto.

READ MORE: Council’s second homes increase not implemented ‘due to Welsh Government review’

Nakamoto later made the software for their new cryptocurrency – Bitcoin, now the most widely used and known cryptocurrency – available for free online.

The idea is rooted in libertarianism, which argues that governments should be small, playing an extremely limited role in the lives and actions of individuals and businesses. As such, libertarians argue in favour of cutting regulations and against large, centralised institutions like banks, the NHS, and food and environmental standards agencies.

") A statue in Budapest dedicated to Satoshi Nakimoto, whose real identity is unknown. (Picture: Elekes Andor)

A statue in Budapest dedicated to Satoshi Nakimoto, whose real identity is unknown. (Picture: Elekes Andor)

Because cryptocurrencies allow people to buy and sell things outside of the banking system – and because the concept is so new – it’s not subject to the same rules as we’re used to having with regular old pounds and pennies.

While this is good news for libertarians, it can also cause problems – as we’ll see.

Bitcoin and the environment

As we’ve covered, this is the most well-known and widely used cryptocurrency.

If you’ve heard of Bitcoin at all, you might also have heard that it’s bad for the environment – that’s because of the PoW.

We know now that a network of computers needs to solve a very complicated puzzle to get the hash that confirms a Bitcoin transaction, and the first computer in that network to find the answer gets rewarded with their own Bitcoin tokens – which can either be used or sold off for traditional money. This process is called Bitcoin mining.

") A cryptocurrency mining farm in Iceland. (Picture: Marco Krohn)

A cryptocurrency mining farm in Iceland. (Picture: Marco Krohn)

As you might imagine, this prospect of “free money” is a big draw, so the Bitcoin mining network has grown substantially over time. In turn, the hash puzzle has become extremely complex, requiring an enormous amount of computing power – and energy – to complete.

The more computing power you have at your disposal, the more likely you are to be the one who solves the puzzle. So Bitcoin miners are incentivised to constantly run huge banks of computers in the hope of getting their reward.

At the time of writing, a single Bitcoin transaction is estimated to have the same carbon footprint as watching Youtube non-stop for about 20 years. Annually, the Bitcoin blockchain reportedly consumes a similar level of electricity as the country of Thailand.

READ MORE: St David’s Day Bank Holiday: lobby Westminster for right

A group of Bitcoin miners in New York recently attracted outrage when they purchased a disused coal power station, reopening it as a gas-fired plant to power their bank of 15,300 computer servers. Similar operations have been reported across the US.

Last summer, meanwhile, West Midlands Police conducted a raid on what they thought was a cannabis factory – only to find a Bitcoin mining operation that had syphoned thousands of pounds of electricity from the Western Power Grid.

Why go to this extreme effort? Because a single Bitcoin is currently worth £32,185.

This high value is the result of a cycle of “hype” and scarcity (see below).

The continuing growth of Bitcoin

The continuing growth of Bitcoin

The value, however, is highly volatile – it can jump up and down by thousands of pounds from one hour to the next.

When Elon Musk announced last year that he’d bought $1.5bn worth of Bitcoin through his company, Tesla, the cryptocurrency’s value rocketed – when, months later, he tweeted a meme suggesting he wasn’t so keen, the price collapsed.

Ethereum and NFTs

Phew – Nearly done!

The Ethereum blockchain, released in 2015, is also used for cryptocurrency – Ether, which at the time of writing is worth just under £3,000 a piece.

Like Bitcoin, Ethereum is highly energy intensive (though to a lesser degree), and the value of Ether is highly volatile.

What Ethereum is most known for, though, is the Non-Fungible Token, or NFT.

READ MORE: Building a business park plan on family farm ‘would create jobs and investment’

Bitcoin and Ether tokens are fungible, meaning that each single token has the same basic value – much like any £5 note has the same value as any other £5 note.

This is not the case for NFTs (hence the name!), and so they can’t be used to make transactions.

The NFT is a unique hash code containing a link (like the ones you see in your browser search bar) to a digital object stored on the internet. This object can be anything, in theory, but is most often artwork – illustrations, songs, or maybe a video clip.

Joined @BoredApeYC ready for the reveal? Thanks @moonpay concierge pic.twitter.com/gzm1JQEHHF

— Gwyneth Paltrow (@GwynethPaltrow) January 26, 2022

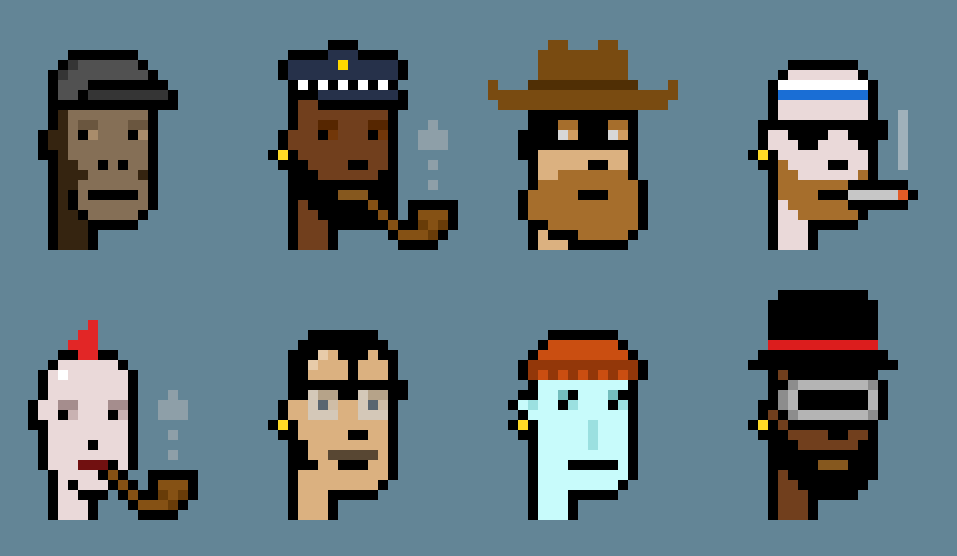

Some of the most popular NFTs are “Bored Apes” – pictures of cartoon apes wearing a range of different outfits. The Bored Ape Yacht Club – a kind of social network for traders of Bored Apes – boasts Gwyneth Paltrow, Snoop Dogg and even former Chelsea football captain John Terry amongst its members.

Boy George released an NFT collection called CryptoQueenz this month, while the Banksy Preservation Society plans to raise funds to purchase Port Talbot’s Season’s Greetings mural by selling “exclusive NFT art drops”.

Designed by Boy George

Would love to hear your thoughts❤️#NFT @theCryptoQueenz ? pic.twitter.com/xoLSU87zVa— TheCryptoQueenz by Boy George (@thecryptoqueenz) February 10, 2022

Manchester City FC has also minted its own range of NFTs.

It’s often said that NFTs are “proof of ownership” of the digital object, but this isn’t strictly true.

Unless the terms of the sale explicitly say otherwise, what you’re buying is a web link to where the object is stored. Blockchains don’t have the capacity to store big files, so the actual piece of art must be stored on an ordinary website (usually the auction site selling the NFT, like OpenSea).

The buyer doesn’t receive a physical copy, doesn’t own copyright, and the creator of the art is free to “mint” (a process which, again, requires huge computing power) more NFTs of the same piece of work.

Think of a nice sports car, stored in a garage: When you buy an NFT, you’re buying directions to that garage, not the car or even the garage itself.

Nevertheless, some NFTs have sold for enormous sums – an NFT of “Merge”, a picture of two planets created by digital artist Pak, sold for $91.8m in December. The high price of NFTs means that often, groups of people pool their Ether in order to make the purchase.

READ MORE: SpaceX lose 40 Starlink satellites after geomagnetic storm

Some NFTs also contain a “smart contract” which will automatically pay the artist royalties if the token is resold.

Once again, the idea here is to circumvent big institutions – an artist can mint an NFT of their work and sell it without needing to display their art at a gallery, or add their music to Spotify.

") An NFT collection released in Turkey this week, purportedly to raise money to restore the country’s bee population in the face of climate change. (Picture: PA Wire)

An NFT collection released in Turkey this week, purportedly to raise money to restore the country’s bee population in the face of climate change. (Picture: PA Wire)

Could the artist also sell their work on a regular website, or at a market? Yes.

The smart contract, though, as an unchangeable record on the blockchain, would automatically pay the artist their royalties without the need to negotiate fees. However those royalties are dependent on finding a new buyer for the NFT, and how much people are willing to pay for it.

NFTs are also mostly bought and sold in Ether, which again, is liable to sudden shifts in value.

READ MORE: ‘ How the cost of living crisis turned levelling up upside down’

The NFT world is also increasingly associated with so-called “rug pulls”, in which buyers pay for tokens that don’t exist, that have no resale value, or contain code that prevents the buyers from selling them at all.

According to software company Chainalysis, rug pulls earned scammers around £2bn last year alone.

A recent study, meanwhile, found that 110 users had successfully made millions through “wash trading” – artificially driving up the value of their NFTs by buying and selling it to themselves for increasingly high prices, in the hope of attracting a genuine buyer.

Betrayed, but not broken.

The Angry Dwarves Tribe is a community-driven NFT project born from the aftermath of the Rich Dwarves Tribe Rug Pull.

We are dedicated to making an open, honest project, and welcome any former Dwarves, as well as all newcomers.

Discord In Bio pic.twitter.com/RZ6dIFcXUK

— angry dwarves (@angrydwarvesNFT) February 11, 2022

In the traditional stock market, this practice has been illegal for years – but as cryptocurrency is still so new and largely unregulated, those who fall foul of rug pulls, wash trading, or indeed any other kind of cryptocurrency fraud, have very little recourse.

John Hawkins, senior lecturer at the University of Canberra’s School of Politics and Economics, wrote recently: “While not illegal, many NFT marketing ventures have some similarities with Ponzi schemes, such as that operated by Bernie Madoff (who sustained his fraud for decades by paying high “dividends” from the deposits of new investors).

“Cryptocurrency markets work in essentially the same manner. For existing investors to profit, new buyers have to be drawn into the market.

“So too NFTs, with something illusory attached to the digital assets.”

“The larger the bubble becomes, the wider the contagion when it bursts,” he concluded.

If you value The National’s journalism, help grow our team of reporters by becoming a subscriber.

Credit: Source link